Japan Market Entry Barriers for Foreign Investors in the Resources and Energy Sector

Market Entry Strategy

Battery Storage

Hydrogen & Ammonia

Renewable Energy

Executive Summary

Japan remains one of the most attractive energy-transition markets in Asia, but it is also one of the most execution-sensitive. The opportunity is driven by scale, import dependence, decarbonization policy, and public support mechanisms for offshore wind, hydrogen, ammonia, batteries, and related infrastructure. The barrier is that entry risk in Japan is cumulative rather than isolated: foreign investment screening, environmental and local permitting, grid economics, supply-chain readiness, and stakeholder management all need to work together for a project or acquisition to be investable. (ANRE, 2025) (NEDO, 2026) (MOF, 2024)

For foreign investors, the most important practical point is that Japan’s market-entry challenge is not simply “regulatory complexity.” It is sequence risk. A deal can clear commercial underwriting and still fail because FEFTA timing was misread, grid curtailment was underpriced, local coexistence was handled too late, or offshore installation capacity could not be secured on viable terms. The more successful pattern is usually staged entry: build or buy a local platform, form a capable consortium, and scale only after the regulatory and operating model is proven in Japan. (MOF, 2023) (OCCTO, 2025) (FSA, 2025) (Reuters, 2025)

Introduction

Japan matters because it combines a large, sophisticated energy market with unusually high strategic urgency. The latest Strategic Energy Plan continues to frame policy around safety plus “3E” goals—energy security, economic efficiency, and environmental suitability—and repeatedly stresses Japan’s structural constraints: limited domestic natural resources, mountainous land, and deep surrounding seas. That policy logic helps explain why Japan is simultaneously accelerating renewable energy, strengthening supply-chain resilience, and tightening oversight over sensitive investment and infrastructure. (ANRE, 2025)

For foreign capital, the attraction is broad rather than narrow. Renewable generation, storage, hydrogen and ammonia, LNG and gas infrastructure, and critical minerals all sit inside long-term industrial and energy-policy agendas. NEDO’s Green Innovation Fund alone was established with an initial JPY 2 trillion and had expanded to JPY 2.7564 trillion as of November 2024, while JOGMEC’s legal mandate has been broadened to include offshore wind geological surveys, hydrogen and fuel-ammonia equity investment, CCS support, and domestic processing and smelting of rare metals. (NEDO, 2026) (JOGMEC, 2022)

The difficulty is that Japan is best understood not as a single market but as three overlapping systems: a security system, a transition system, and a compliance system. Investors therefore need a Japan entry strategy that reconciles national-security screening, long permitting cycles, liberalized electricity-market exposure, local language and consensus requirements, and increasingly explicit carbon-pricing obligations. (MOF, 2024) (ANRE, 2023) (METI, 2025)

Key Takeaways

Japan’s main entry barrier is not one approval but a chain of approvals and operating constraints: FEFTA screening, EIA and permits, grid connection, revenue model, and supply chain. (MOF, 2023) (MOE, n.d.)

In designated sectors, prior notification can apply at 1% of a listed company or any shares in an unlisted company, with a 30-day standstill that can be extended to four months. (MOF, 2023) (MOF, 2024)

Energy and resource-related sectors remain sensitive under FEFTA, and Japan updated designated-sector coverage again in 2024, including critical minerals, semiconductor-related equipment, marine engines, and related supply-chain items. (MOF, 2024)

Renewable bankability now depends heavily on post-FIT commercial design. Japan’s FIP scheme started in April 2022, and IEEJ identifies FIP/PPA business models as a central challenge in the post-FIT environment. (ANRE, 2023) (IEEJ, 2024)

Grid congestion and curtailment are critical underwriting variables: OCCTO reports 388 renewable-curtailment instructions in FY2024, 83 more than FY2023. (OCCTO, 2025)

Offshore wind remains strategic, but 2025 project withdrawals showed that inflation, interest rates, weak supply chains, and Japan-specific execution risks can overturn auction economics. (ANRE, 2025) (Reuters, 2025) (IEEJ, 2024)

For hydrogen and ammonia, partnership with Japanese utilities or industrials is becoming more relevant as support moves from concept to implementation; JOGMEC’s 2026 subsidy support for JERA’s low-carbon ammonia supply plan is one visible example. (JOGMEC, 2026)

The best-performing entry model is usually partner-led, with strong authorship of the local operating plan: local developer or utility relationships, conservative contracting, and explicit treatment of Japan-specific interface risk. (FSA, 2025) (IEEJ, 2024)

Market Overview

Japan’s resources and energy market can be simplified into three layers. First is the security layer: imported fuels and strategic minerals remain essential, so energy policy is inseparable from economic security. Second is the transition layer: renewable power, storage, hydrogen, ammonia, CCS, and electrification are backed by national policy and public funding. Third is the market layer: liberalized power markets, FIP support, corporate PPAs, and new GX-related compliance mechanisms are pushing investors toward more active revenue and risk management. (ANRE, 2025) (ANRE, 2023) (NEDO, 2026) (METI, 2025)

That structure means foreign investors should choose entry mode as carefully as they choose technology. A minority platform investment, a control acquisition, a consortium bid, and a greenfield project each face different approval pathways and different sensitivities to FEFTA, EIA, curtailment, port access, or local consensus. (MOF, 2024) (JETRO, 2025)

Subsector / entry target | Regulatory approvals and recurring compliance gates | Typical timeline | Key agencies | Common deal structures |

|---|---|---|---|---|

Acquisition of a Japanese energy or resource company | FEFTA prior notification where applicable; transaction and post-investment reporting; sector diligence | 1–4 months for straightforward cases; longer if review extends | MOF, METI, competent ministry | Minority platform stake, staged control acquisition, full acquisition with FEFTA conditions precedent |

Utility-scale solar / onshore wind | FIT/FIP business plan certification; grid interconnection; local permits; EIA where triggered | 2–5+ years | ANRE/METI, MOE, local governments, OCCTO, GT&D companies | RTB acquisition, local developer JV, corporate PPA structure |

Offshore wind | Zone designation; council process; auction qualification; marine and EIA steps; port/vessel compliance | 5–10+ years | METI, MLIT, MOE, local governments, OCCTO | Consortium bid, utility or trading-house JV, project-finance SPV |

BESS / flexibility assets | Interconnection; market registration; balancing and capacity-market eligibility | 1.5–4 years | ANRE/METI, OCCTO, EGC | Co-located storage, merchant-plus-capacity SPV, developer platform |

LNG / hydrogen / ammonia facilities | FEFTA where relevant; gas and safety approvals; High Pressure Gas compliance; local land and port approvals | 3–7+ years | METI/ANRE, local authorities, JOGMEC, sector regulators | Strategic JV, tolling or throughput model, trader-offtaker consortium |

Critical minerals processing / recycling | FEFTA sensitivity; environmental permits; industrial safety approvals; supply-chain and security diligence | 2–6+ years | MOF, METI, MOE, local authorities | Industrial JV, offtake-backed investment, processing platform |

Table note: timeline ranges are indicative market-practice estimates synthesized from official approval pathways and recent market experience; actual durations vary by prefecture, EIA scope, connection queue, and transaction structure. Sources include MOF, MOE, OCCTO, FSA, ANRE, and JETRO.

Challenges

The first challenge is legal and national-security screening. FEFTA’s thresholds are low by international infrastructure-investor standards, and the range of covered actions is wider than a simple share acquisition. MOF’s own materials make clear that prior notification can apply to 1% or more of a listed company, any shares in an unlisted company, and certain governance or business-change actions. It is equally important that the designated-sector list has continued to expand in response to economic-security concerns, including critical minerals and specified critical products. For foreign investors, that means transaction design, governance rights, and timeline control all need to be structured from the start—not after exclusivity. (MOF, 2023) (MOF, 2024)

The second challenge is regulatory sequencing and permitting duration. Japan’s environmental-impact framework is formal, document-heavy, and often long-dated. At the same time, offshore wind procedures are evolving: in 2025 the government moved to permit development in Japan’s EEZ and to incorporate marine-environment surveys earlier in zone designation. That is strategically positive, but it also front-loads more process and more diligence before revenue certainty exists. In practice, investors need to underwrite a moving process environment, not a static one. (MOE, n.d.) (METI, 2025)

The third challenge is commercial and financial viability in a post-FIT, high-cost environment. ANRE’s own material confirms that FIP has been in force since April 2022, while IEEJ identifies FIP/PPA model design, community coexistence, and location scarcity as the central renewable-policy challenges. That matters because Japan entry is no longer bankable on tariff assumptions alone. Revenue, balancing, curtailment, and refinancing all matter more than they did under legacy FIT logic. Offshore wind made this visible in 2025, when Mitsubishi withdrew from three awarded projects because of soaring costs. (ANRE, 2023) (IEEJ, 2024) (Reuters, 2025)

The fourth challenge is grid and technical bankability. OCCTO’s FY2024 figures confirm that curtailment is now a national issue, not a local anomaly. At the project level, wind developers must also screen for radar and defense constraints. The 2024 wind-interference law introduced notification obligations, zoning, and potential construction restrictions in areas affecting Self-Defense Forces radio operations. This creates a category of hard-stop technical risk that can destroy value if left until late-stage development. (OCCTO, 2025) (Japanese Law Translation, 2025)

The fifth challenge is cultural and stakeholder coordination. In Japan, community acceptance is not a soft issue; it is often a project-defining variable. IEEJ explicitly highlights the need to build consensus with local communities, while ANRE’s offshore-wind framework depends on formal local coordination through statutory councils. For foreign sponsors, this means that Japanese-language documentation, municipal coordination, fisheries engagement, and patient local process management are not ancillary workstreams—they are core execution disciplines. (IEEJ, 2024) (ANRE, 2025)

The sixth challenge is supply-chain depth and industrial readiness. IEEJ’s offshore-wind work argues that Japan has strong industrial potential in shipbuilding, marine civil engineering, and submarine cable technology, but still needs scale, cost reduction, and market clarity to attract global OEM commitment. FSA’s 2025 policy package also shows that vessel availability was serious enough to trigger nationwide regulatory changes on the use of foreign-flag ships for installation and maintenance. In other words, Japan’s offshore bottleneck is partly industrial and partly regulatory. (IEEJ, 2024) (FSA, 2025)

The seventh challenge is policy volatility under security stress. Japan’s long-term direction is toward decarbonization, but 2026 reporting shows that emergency supply shocks can still force temporary fuel-switching and thermal-policy adjustments. Reuters reported that METI would relax rules for one year from April 2026 to allow greater coal-fired operation amid LNG disruption risk. For foreign investors, that is a reminder that Japan’s market can change quickly when energy security is threatened, especially in fuels, thermal generation, and industrial decarbonization chains that still depend on gas imports. (Reuters, 2026) (ANRE, 2025)

Strategy / Solution

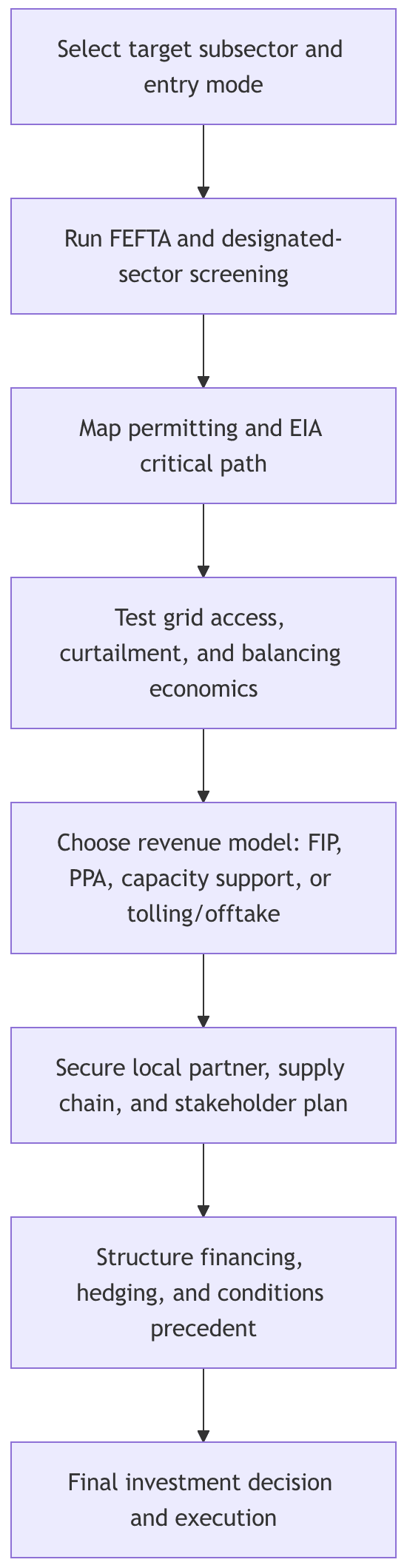

The most robust way to enter Japan is to build a sequenced, partner-led, Japan-specific entry model. In practical terms, that means screening a target or project under FEFTA before valuation is finalized, mapping the permitting critical path before the bid is locked, designing the revenue model around FIP/PPA and curtailment realities, and partnering early with the parties that control stakeholder access, grid knowledge, and supply-chain execution. For hydrogen and ammonia, it also means tracking how public support is actually being deployed rather than assuming that policy intent alone makes a project bankable. JOGMEC’s 2026 support for JERA’s low-carbon ammonia plan is a good illustration of the market moving from concept toward operational support structures. (MOF, 2023) (OCCTO, 2025) (JOGMEC, 2026)

A practical step-by-step approach is as follows. First, choose the right entry archetype: platform acquisition for speed, consortium/JV for legitimacy and execution sharing, or greenfield only where the sponsor already has Japanese operating capability. Second, complete FEFTA triage before signing, not after. Third, create one integrated approval map that includes EIA, local ordinances, grid milestones, port or land-use rights, and security-related siting screens. Fourth, size debt and equity against downside curtailment, balancing costs, and delayed COD risk. Fifth, use contracts that absorb Japan-specific inflation and interface risk: indexed EPC terms, vessel reservations, clear responsibility matrices, and long-stop dates that reflect real regulatory timing. Sixth, for hydrogen, ammonia, and critical minerals, bias toward shared-risk structures with Japanese utilities, traders, or industrial offtakers rather than fully standalone entry. (MOF, 2024) (ANRE, 2023) (FSA, 2025) (JOGMEC, 2022)

Pre-bid checklist

Confirm whether the target or project touches FEFTA designated or core sectors. (MOF, 2024)

Build a single critical-path schedule covering EIA, local approvals, grid milestones, and transaction CPs. (MOE, n.d.)

Stress-test curtailment, merchant-price, balancing, and refinancing assumptions before IC approval. (OCCTO, 2025)

Screen wind sites for defense/radar, fisheries, and local-consensus constraints before site commitment. (Japanese Law Translation, 2025) (ANRE, 2025)

Check vessel, port, and foreign-flag or foreign-worker execution constraints for offshore projects. (FSA, 2025)

Align financing structure with reality: conservative contingencies, indexed contracts, and realistic long-stop dates. (Reuters, 2025) (IEEJ, 2024)

Investor type | Recommended entry strategy | Preferred partnership model | Financing and risk focus |

|---|---|---|---|

Infrastructure fund | Enter through a platform or portfolio acquisition, then scale selectively into development | Local developer/operator JV or staged control acquisition | FEFTA conditions precedent, curtailment-adjusted cash flow case, inflation and refinancing buffers |

IPP / developer | Combine local team build-out with selective M&A and targeted greenfield development | Utility, EPC, OEM, and balancing-counterparty alliances | FIP/PPA optimization, interconnection queue strategy, construction interface risk |

Commodity trader / integrated energy company | Combine fuels, logistics, storage, and downstream offtake in one Japan strategy | Utility, industrial offtaker, trader, and JOGMEC-linked ecosystem | Long-term offtake, safety-compliance, geopolitical and shipping downside planning |

Table note: this strategy matrix assumes unspecified investor nationality, project size, and risk appetite, and is intended for institutional rather than passive investors. It is a deal-structuring synthesis based on official policy and market evidence.

Conclusion

Japan is open to foreign capital, but it is not a low-friction entry market. The real barrier is not foreign ownership by itself; it is the need to align security screening, permitting, grid economics, local trust, and supply-chain execution. That is why foreign investors who treat Japan as “just another OECD market” often misprice the early-stage risk, while those who build local capability and sequence risk properly tend to outperform. (MOF, 2024) (ANRE, 2025) (IEEJ, 2024)

The strongest investment thesis in Japan today is therefore not simply “Japan needs capital.” It is that Japan rewards capital that arrives with transaction discipline, local operating credibility, and a realistic view of timing. In 2026, winning in Japan means underwriting FEFTA, curtailment, community coexistence, offshore supply-chain viability, and carbon-price exposure as primary value drivers rather than secondary diligence items. (OCCTO, 2025) (Reuters, 2026) (METI, 2025)

CTA

If your organization is evaluating acquisition, JV, auction, or greenfield entry into Japan’s resources and energy sector, [Firm Name] can help structure the decision from first screening to executable strategy: regulatory mapping, partner identification, bid posture, and bankability review tailored to Japan’s current policy and operating environment. (MOF, 2023) (ANRE, 2025) (JETRO, 2025)